Increasingly we hear we are in danger of our falling off a “fiscal cliff.” As legislation currently stands the Congressional Budget Office estimates that the Federal budget deficit will fall by $607 billion due to $407 billion in tax increases and automatic spending cuts of approximately $200 billion. Most of the economic and financial intelligentsia operating within a Keynesian framework are very worried that such fiscal changes, while reducing the budget deficit, will push us off a cliff into severe recession viewed as a significant reduction in GDP.

I would suggest that, due to economic reality, the nasty budgetary situation in which we find our nation has already pushed us off a fiscal cliff. Decades of fiscal mismanagement leave us with very few painless options. Our rulers and their intellectual supporters have rejected economic wisdom to such a degree that it amounts to a rejection of reality.

By economic reality, I mean the fundamental facts of economic life. For example, most people, with the exception of modern macroeconomists it seems, understand and accept the existential economic fact of scarcity. There are not enough goods to satisfy all of our ends. Even the Rolling Stones recognized that you can’t always get what you want.

Drawing on economic and philosophical thought developed in light of the nature of human interaction, our best economic thinkers for centuries have generally recognized that economic prosperity requires productive activity. Men like John Baptiste Say, Francis Wayland, Frederic Bastiat, Condy Raguet,

Wilhelm Ropke, Ludwig von Mises, Hans Sennholz, and Murray Rothbard understood that such activity is most fostered by a free society built on private property. State intervention in the economy, therefore, was seen as generally destructive, because the government does not really produce anything. It consumes. Therefore, it is prudent for the magistrate to be strictly limited and to live within its means.

How did we get here from there? Since the middle of the 20th Century, our rulers supported by a growing segment of the intellectual class have taken leave of their economic senses. Since the end of WWII,

increases in government spending have occurred virtually unchecked. Only three times since 1946 did total government spending decline. In 1954 and ’55 it fell because of a cutback in defense spending after the Korean War and in 2010 outlays decreased ever so slightly as TARP spending was phase out of and Obama’s stimulus plan had run its course. Occasionally defense spending fell slightly, but Social Security and Medicare spending has never decreased even once.

Since the early 1970s, tax revenues generally have not kept pace with government spending. With the exception of four years during the Clinton Administration, the federal government has spent more than it has taken in according to its official budget. Of course, with off-budget spending taken into account, spending exceeded revenues through Clinton’s presidency. Since 1970 real government spending has increased a total of 295%. During that same time, government revenue has increased only 156%

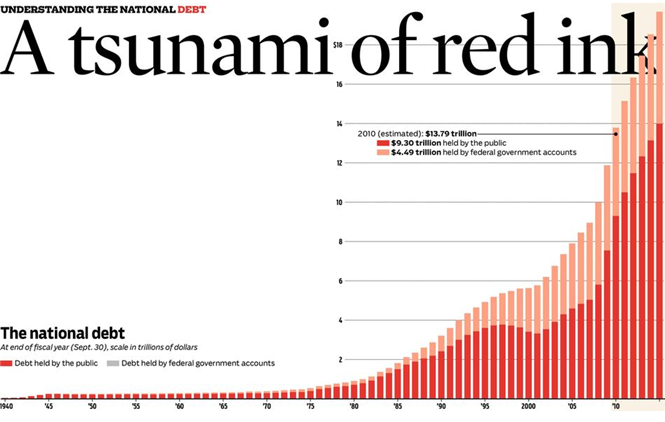

It does not take a PhD from MIT to expect that, given our lack of fiscal discipline, we must have had an almost continual increase in government borrowing. Such a conclusion would be correct. In 1970 our total government debt equaled $381 billion. Yesterday it past the $16 trillion mark. That’s

trillion with a

t. Even if we adjust for inflation, federal government debt has increased over 8 times what it was in 1970.

The trouble, of course is that this debt must be paid back somehow. Either future generations must be taxed more heavily or the Fed merely monetizes the debt so that overall prices kiss the sky and the value of the dollar plummets. This amounts to implicit debt repudiation. The debt gets paid back, but with dollars that may be almost worthless. The only other alternative is

explicit repudiation, which the political class finds impolite even to think about.