Word on the street is that "

inflation cooled in March." That is because, as has now become a mantra, while food and energy prices continue to increase, so-called core inflation, the prices of everything else in the market basket, has remained "

subdued." Indeed, so subdued that David Levy has said Ben Bernanke is exactly right to

ignore price inflation.

As I have said before, however, things are

not as rosy as

we are being told. Normal people, who live their lives outside the beltway know that the prices of the goods they want to buy are generally rising. Mises alludes to the market alertness of the household in

Human Action.

A judicious housewife knows much more about price changes as far as they affect her own household than the statistical averages can tell. She has little use for computations disregarding changes both in quality and in the amount of goods which she is able or permitted to buy at the prices entering into the computation. If she "measures" the changes for her personal appreciation by taking the prices of only two or three commodities as a yardstick, she is no less "scientific" and no more arbitrary than the sophisticated mathematicians in choosing their methods for the manipulation of the data of the market (p. 224).

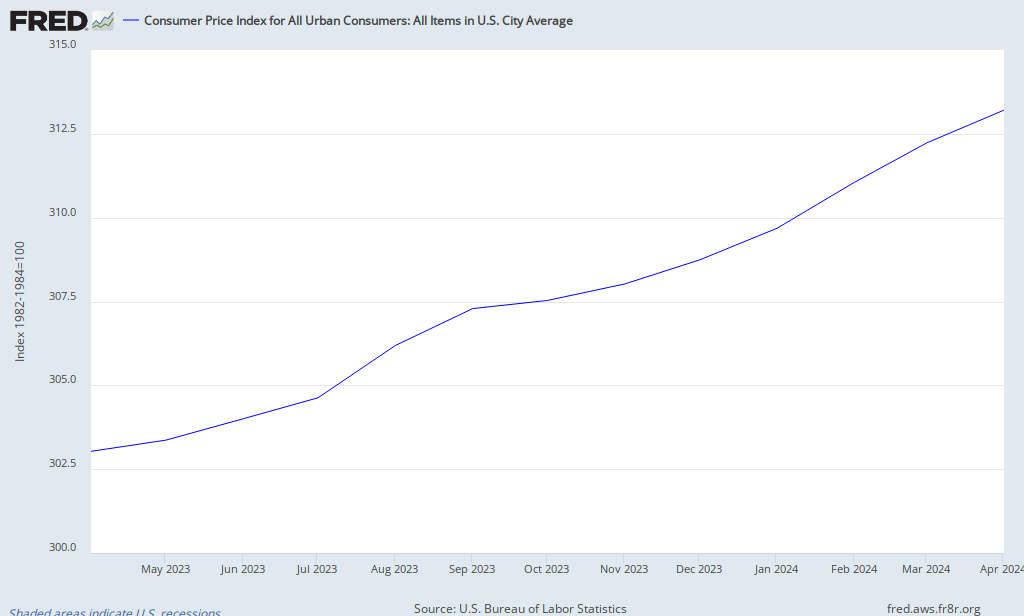

Last month, the

CPI rose 0.5%. If it continues at this rate, price inflation would increase 6% over the next year. That is nothing at which to yawn.

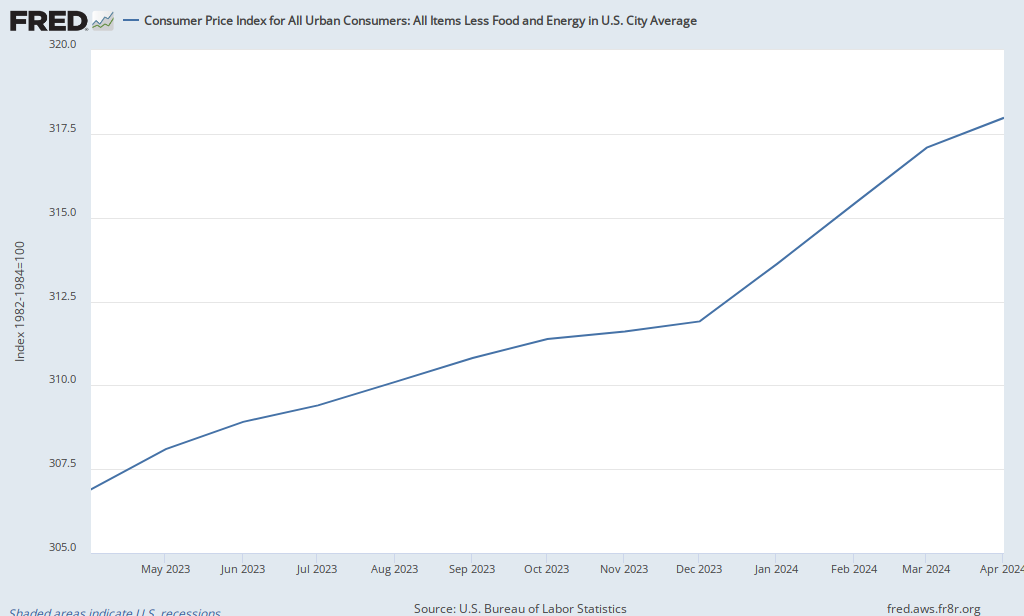

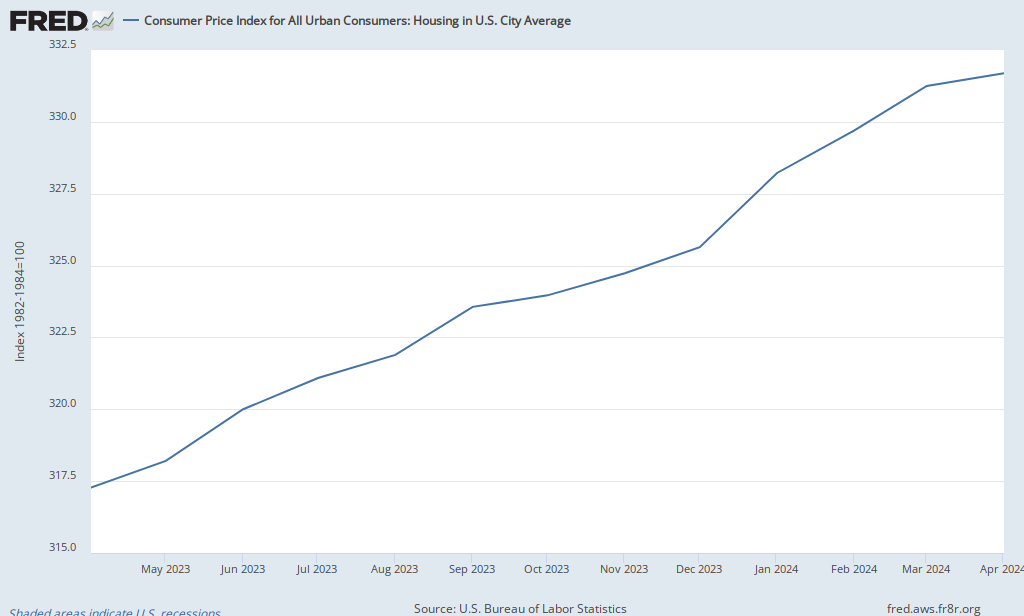

The fact of the matter is that core CPI is rising at a relatively low rate, 0.1% in March, because of the housing market. Prices related to shelter make up 31% of CPI. So

many houses and apartments were made during the housing bubble, housing

prices are flat or falling almost everywhere you look.

However, this does not decrease the cost of living for those people who are staying put. Those who do not need to buy a house are not helped by lower housing prices, especially if prices on everything else are rising.

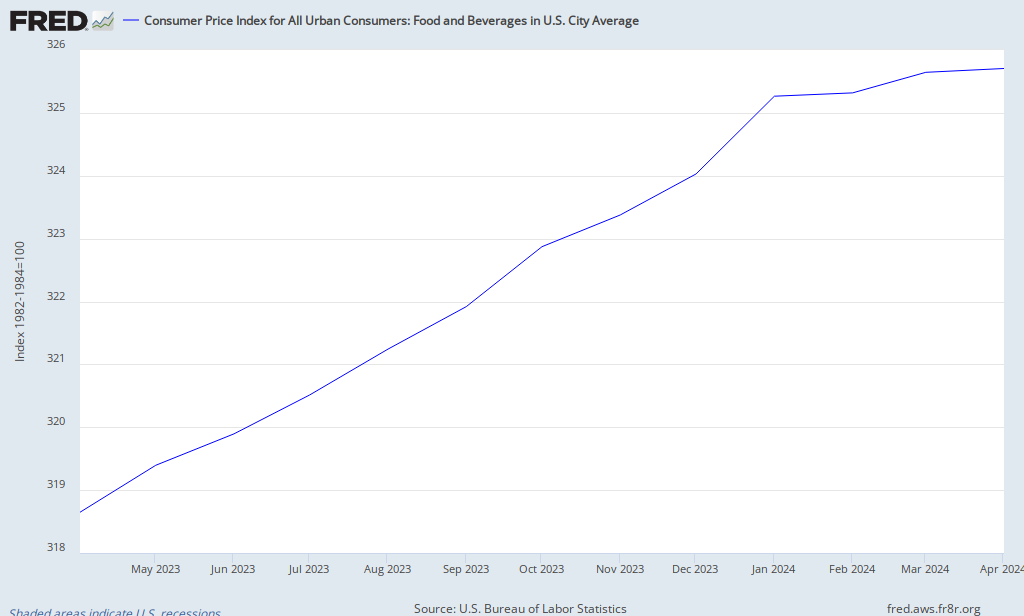

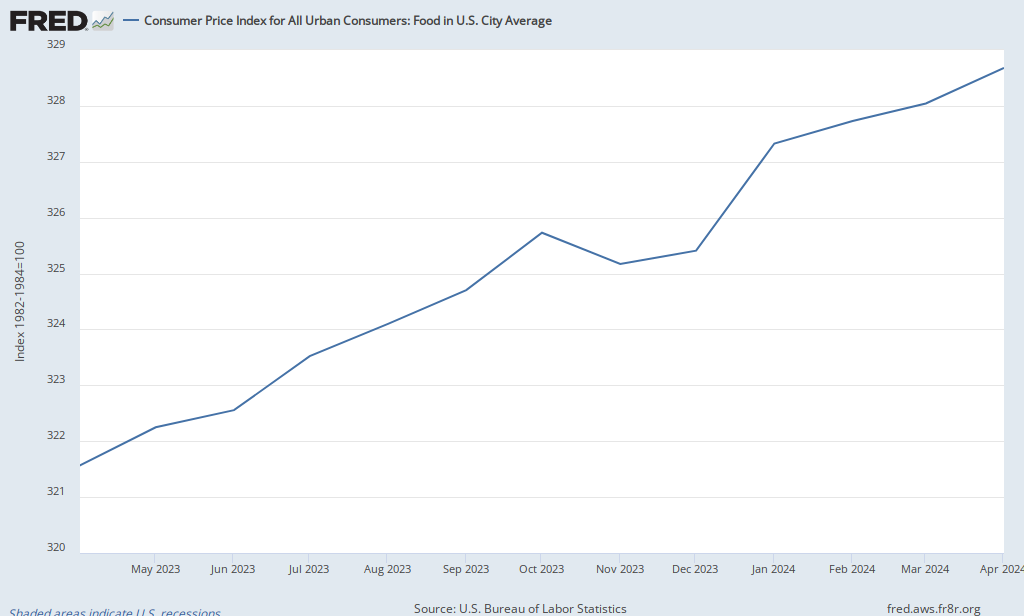

And indeed they are. Food and beverage prices increased at an annual rate of 8.4%.

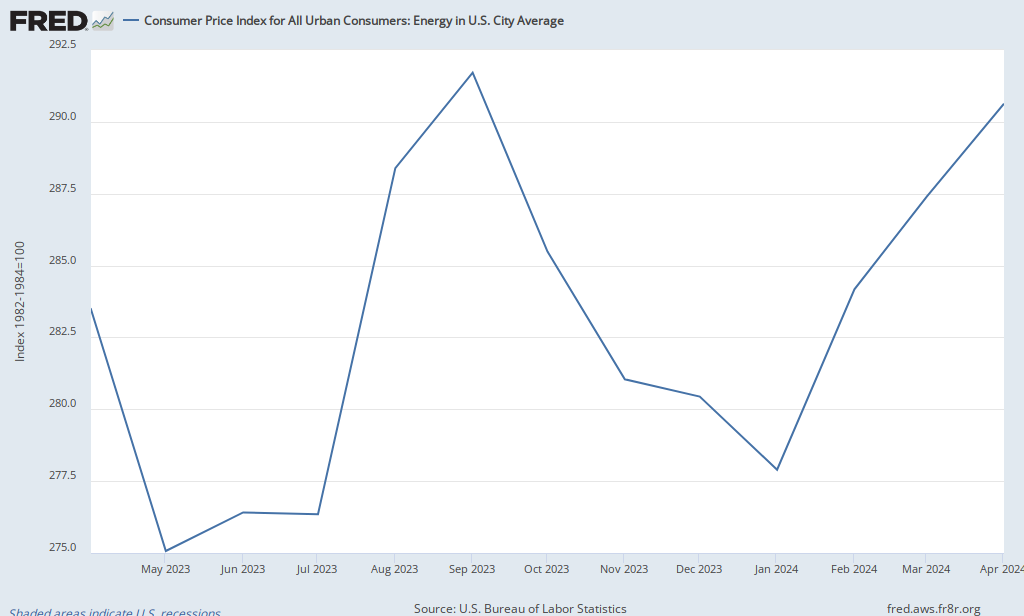

Prices of household fuel and utilities, the part of housing goods that does affect everyone, rose at an annual rate of 7.2%. Transportation prices, which include prices of automobiles, gasoline, and public transportation, rose at an annual rate of 26.4%.

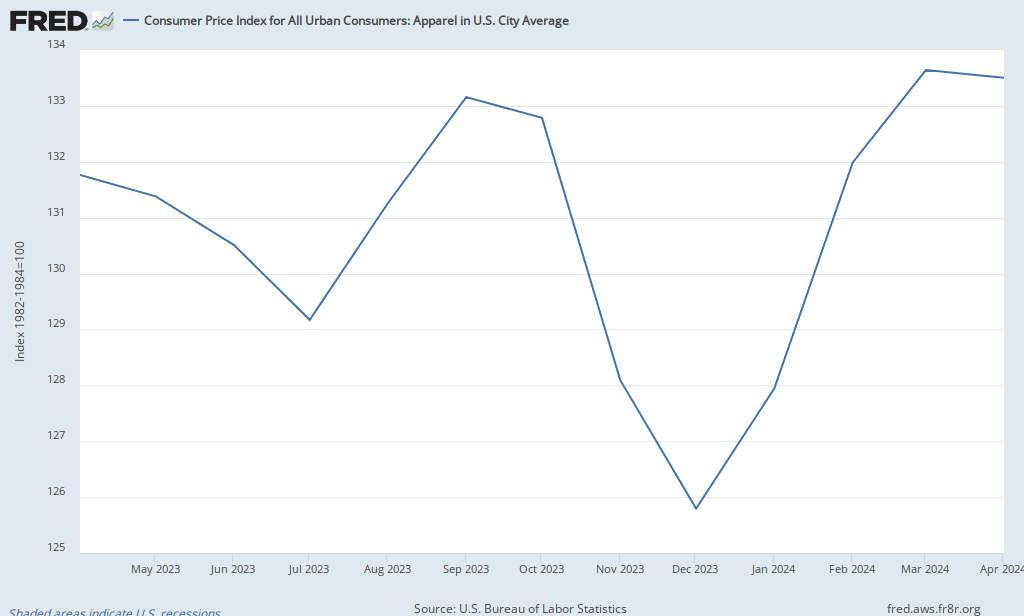

The rise in medical care prices was relatively low at an annual rate of 2.4%. The only truly bright spot for households in which income is tight was that prices for clothing fell at an annual rate of 6%.

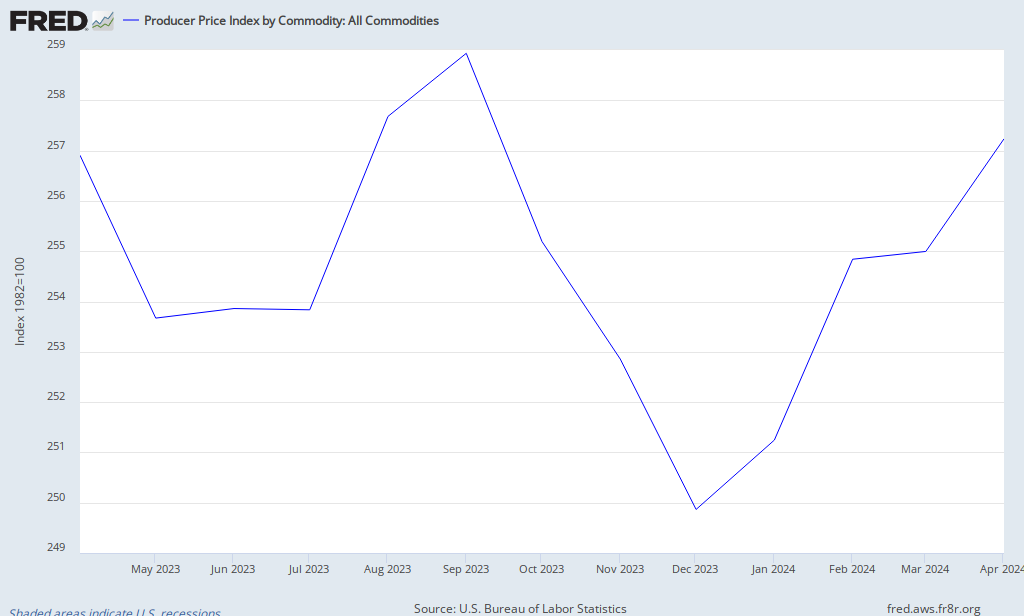

Prices of wholesale goods are also

on the rise. The producer price index increased 0.7% last month, which implies an annual inflation rate of 8.4%.

Randall Holcombe is right to remind us that we should be careful about making long-term predictions based on a single month's data. But as he notes, "

the trend is up."

Looking at the past year, the CPI has increased 2.7% from March 2010 to March 2011. But most of that increase has been recent. In the seven months from March 2010 through October 2010 the CPI rose 0.5%. The five months from October 2010 to March 2011 saw the CPI rise by 2.2%. That’s a 5.3% annual rate of inflation over the past five months.

Finally, there is some stirring of concern amongst some members of the Federal Reserve. Philadelphia Fed President Charles Plosser is now talking about

taking the foot off the monetary accelerator. Richmond Fed President Jeffrey Lacker warns that the Fed

should not be too slow to tighten monetary policy. Unfortunately he is not a voting member of the Federal Open Market Committee (the Fed committee that controls monetary policy) this year. Kansas City Fed President Thomas Hoenig said recently that

interest rate hikes should come soon. Chicago Fed President Charles Evans, however, is still content with the conventional wisdom that "

underlying inflation is still low."

Of course, none of this price inflation had to happen. The Fed did not have to act to engage in any money printing at all. All of the above cheered on past monetary inflation. If they instead allowed capital malinvestment to be liquidated, the economy would be in better shape now than it is. And we would not have to be reporting higher prices everywhere except in housing and apparel.