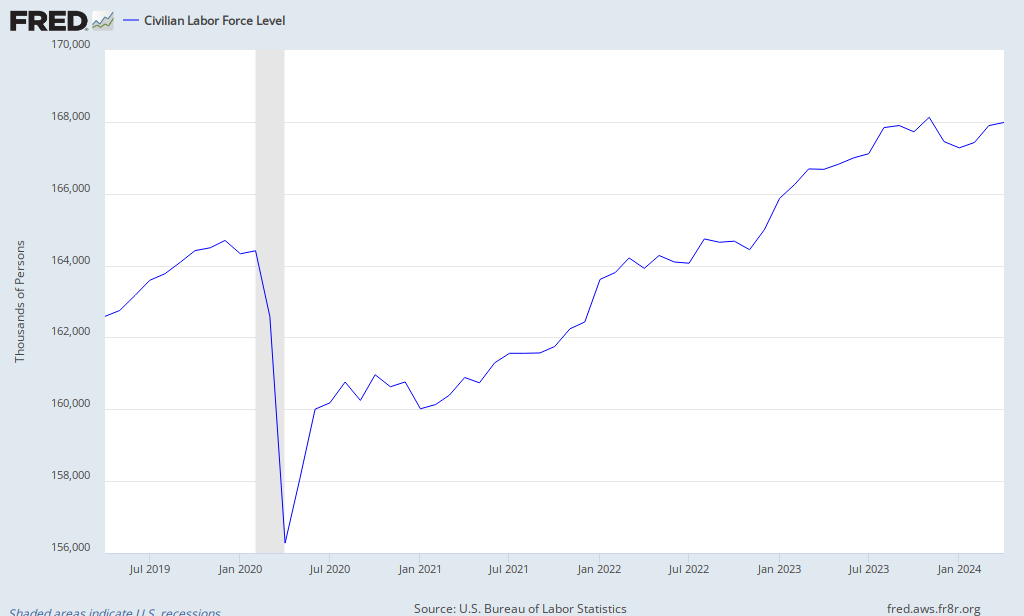

To its credit, in the official labor report, the BLS itself takes a rather measured tone. In the first two pages of the news release the phrases "little changed" or "changed little" are used seven times. The best news in Friday's labor report was that private sector jobs increased by 230,000. Any sustained recovery will be the result in productive activity coordinated by private entrepreneurs. A nation cannot pave the road to prosperity with government jobs. Still, an important reason that the official rate is not a lot higher is that the civilian labor force is still lower than just a year ago and way down from its peak in 2008. If fewer people are actively looking for work, the unemployment rate will decline, even if the number of jobs remains the same.

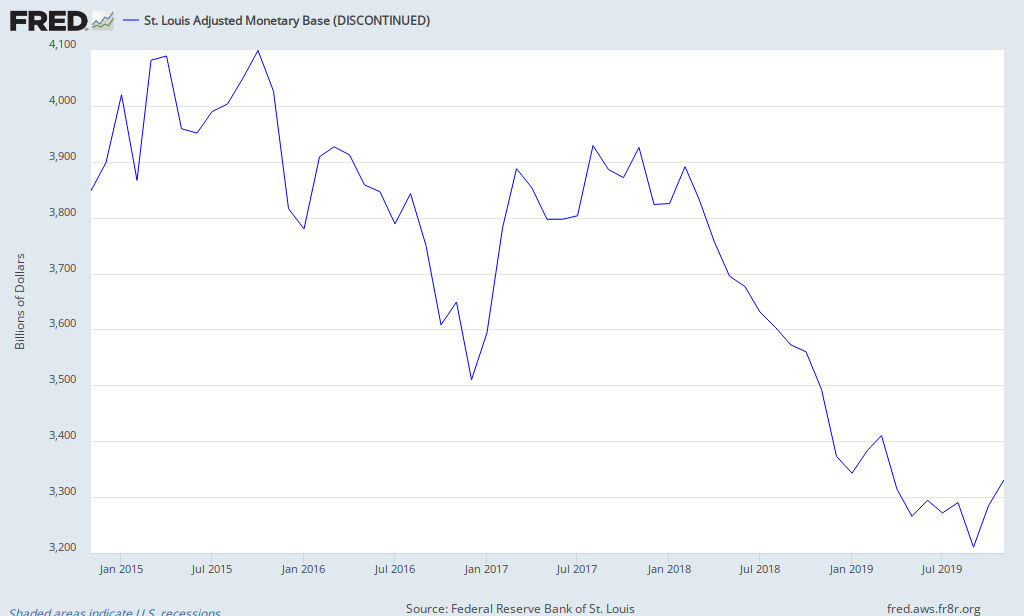

Even given the news of increased private sector employment, however, it is disheartening to hear people interpret the recent drop in unemployment as vindication for Money Printing 2 and Obama's fiscal stimulus. There is, of course, a superficial post hoc, ergo propter hoc plausibility. After all, the Fed did increase the monetary base by over a trillion dollars.

And the national government has increased federal spending so much that it has made annual budget deficits above a trillion dollars the new normal.

Nevertheless, people who make the claims that such monetary and fiscal expansion have sown the seeds of recovery do so because they do not understand capital theory. Certainly an increase in government spending funded by debt financed by monetary inflation can stimulate a lot of activity. As Austrian economists since Ludwig von Mises have explained, monetary inflation via credit expansion can encourage investment in long-term capital intensive production projects. Those entrepreneurs who get the new money first will use their new purchasing power to demand more labor, bidding some workers away from other employers and other workers out of idleness by offering higher wages. In such circumstances the unemployment rate can fall.

Eventually, however, economic reality prevails, revealing that the new funds available to entrepreneurs were not due to increased savings, but pure monetary inflation. In other words, the capital structure has been distorted via malinvestment. Once it becomes apparent that there is not enough real savings to fund the real capital investment necessary to complete all of the new longer-term projects begun, recession sets in, businesses who cannot make it must liquidate and unemployment will rise again.

It is entirely possible, indeed likely, that much of whatever improvement there has been in the labor situation is not sustainable because it has been funded by artificial stimulus. Productive employment, precisely because it is truly productive, does not need to be propped up by inflation and government spending. It is the result of productive investment funded by real voluntary savings.

No comments:

Post a Comment