Irwin Keller at MarketWatch thinks so. As MSM reports:

Kellner compares this kind of stimulus to President Roosevelt's Works

Progress Administration. "The fact that more money was in circulation

resulted in more income, spending, jobs and eventually more purchases of

capital goods by business," he adds. "While it lasted, it helped us

climb out of the depths of the Great Depression."

Can this expand the economy?

Keller is so wrong. It is maddening that we have our economic intelligence insulted like this every time a disaster hits. It is no doubt true that some forms of spending increased and will continue to increase as people rebuild from destruction by the hurricane. That does not mean, however, that people are left more wealthy or that the economy will be more healthy.

Henry Hazlitt, in his Economics in One Lesson, has a more accurate take on such assertions by applying Bastiat's example of the broken window fallacy to the supposed blessings of destruction. "No man burns down his own house on the theory that the need to rebuild it will stimulate his energies" (p. 27). "Plants and equipment cannot be replaced by an individual or a socialist government) unless he or it has acquired or can acquire the savings, the capital accumulation, to make the replacement. But war [or a hurricane] destroys accumulated capital" (p. 30).

Hazlitt was also provides a more accurate assessment of the economic efficacy of the WPA. "When we had our WPA, it was considered a mark of genius for the administrators to think of projects that employed the largest number of men in relation to the value of the work performed--in other words, in which labor was least efficient" (p. 72).

Even if the destruction wrought by Hurricane Irene causes some people to increase spending on construction and, therefore, not hold as much cash as they otherwise

would (Keynes' unpardonable sin of hoarding), they are still left

worse off, because they would rather hold a certain cash balance that

they now cannot because they must make house repairs.

Bloomberg's "Inside Track" provide a sketch of where the money went when Bernanke's Fed went on its lending binge from August 2007 through April 2010. The numbers are, well, numbing. And it was not just American banks who were lining up for the cash. Several industrial companies got Fed money and billions wer even lent to foreign banks.

"Inside Track" reports that "The largest borrower, Morgan Stanley, got as much as $107.3 billion, while Citigroup Inc. took $99.5 billion and Bank of America Corp. $91.4 billion. . . ." It is moves like this that enshrines 'too big to fail" as national policy.

CNN reports that the USDA is making a special purchase of $40 million worth of chicken in an effort to bailout chicken farmers. The goal is to absorb a substantial excess supply of poultry. "Total chicken production in the first half of 2011 rose 4% compared to

the same period a year ago, while demand for chicken has cooled,

according to the National Chicken Council." Lower prices due to increased supply coupled with higher costs of production has put many poultry farmers in a rather tight financial situation.

Why did chicken production increase 4% over the past year even though costs rose noticably? An important part of the reason is government subsidies. CNN reveals:

The government made a similar move with a $30 million purchases of chicken products last year and a $42 million purchase of chicken products on 2008 with the intention of stabilizing retail prices.

In a free society those who cannot profitably operate in an industry must either liquidate their capital or direct it toward more productive uses. Instead, the USDA hampers the market and resources are mis-allocated such that more scarce factors of production are directed toward chicken production than people in society desire. Scarce land, labor, and capital are hampered from being invested in more highly valued uses. That is nothing to crow about.

Too much attention is paid to Rick Perry in this interview, but kudos to Aaron Trask for noting that the one who the great Stockman agrees with about the Fed is Ron Paul. The title of the video should be "Ron Paul Is Right the Fed is Totally Wrong." Stockman makes several great points that need to be repeated again and again and again. The Fed is "utterly destroying our capital markets," and the main reason our economy is still stagnate. "The fact is the Fed is the number one problem holding back this

economy, punishing savers, savaging low income people trying to buy

food, energy or fuel."

Money is not neutral. The premise of the neutrality of money asserts that when the stock of money changes, the only result is a change in overall prices, such that real economic conditions remained unchanged. It has been argued, therefore, that all of this monetary inflation we've had over the past several decades has had no real negative impact on standard of living for people. Prices have rise, but so has our monetary incomes, so we are left no worse off.

While it is true that there is no general social benefit from monetary inflation, it is not true that money is neutral. As Mises explains the consequences of monetary inflation:

The additional quantity of money does not find its way at first into the pockets of all individuals; not every individual of those benefited first gets the same amount and not every individual reacts to the same additional quantity in the same way. Those first benefited? In the case of gold, the owners of the mines, in the case of government paper money, the treasury now have greater cash holdings and they are now in a position to offer more money on the market for goods and services they wish to buy. The additional amount of money offered by them on the market makes prices and wages go up. But not all the prices and wages rise, and those which do rise do not rise to the same degree. If the additional money is spent for military purposes, the prices of some commodities only and the wages of only some kinds of labor rise, others remain unchanged or may even temporarily fall. They may fall because there are now on the market some groups of men whose incomes have not risen but who nevertheless are obliged to pay more for some commodities, namely for those asked by the men first benefited by the inflation. Thus, price changes which are the result of the inflation start with some commodities and services only, and are diffused more or less slowly from one group to the others. It takes time till the additional quantity of money has exhausted all its price changing possibilities. But even in the end the different commodities are not affected to the same extent. The process of progressive depreciation has changed the income and the wealth of the different social groups. As long as this depreciation is still going on, as long as the additional quantity of money has not yet exhausted all its possibilities of influencing prices, as long as there are still prices left unchanged at all or not yet changed to the extent that they will be, there are in the community some groups favored and some at a disadvantage. Those selling the commodities or services whose prices rise first are in a position to sell at the new higher prices and to buy what they want to buy at the old still unchanged prices. On the other hand, those who sell commodities or services whose prices remain for some time unchanged are selling at the old prices whereas they already have to buy at the new higher prices. The former are making a specific gain, they are profiteers, the latter are losing, they are the losers, out of whose pockets the extra-gains of the profiteers must come. As long as the inflation is in progress, there is a perpetual shift in income and wealth from some social group, to other social groups. When all price consequences of the inflation are consummated, a transfer of wealth between social groups has taken place. The result is that there is in the economic system a new dispersion of wealth and income and in this new social order the wants of individuals are satisfied to different relative degrees, than formerly. Prices in this new order can not simply be a multiple of the previous prices.

This phenomena is being played out right now in front of our very eyes. The New York Times reports that sales of luxury goods are recovering strong, even with price mark ups! Notice this very revealing passage pinpointing the cause of the new luxury good boom:

What changed? Mostly, the stock market, retailers and analysts said, as well as a good bit of shopping psychology. Even with the sharp drop in stocks over the last week, the Dow Jones is up about 80 percent from its low in March 2009. And with the overall economy nowhere near its recession lows, buying nice, expensive things is back in vogue for people who can afford it.

Perhaps the above thinking is partly to explain Bernanke's recent pronouncement of future monetary profligacy. If the Fed can bolster equity prices again, consumer spending will be further stimulated and the "economy" will receive the elusive "jump start" the Fed has been trying to initiate. Of course, on the other hand, pesky reality and economic law will continue to assert themselves.

Here is the great Jeffrey Herbener, who happens to be my department chairman, lecturing on "Subjective Value and Market Prices." This lecture is from this summer's Mises University and is a good example of how economic theory is developed in classes at Grove City College.

The main explanation Keynesians offer for unemployment when there is a drop in what they call aggregate demand is that wages are "sticky downward." That is, even though demand for labor falls, something prevents wages from falling to market clearing levels. If wages are kept above the market level, their will be a surplus of labor, or unemployment. Lower aggregate demand plus sticky wages equals mass unemployment, QED.

Manfred Honneck and the Pittsburgh Symphony Orchestra

I have already written, however,about how rigid wages are not a universal problem. Another more recent example of falling wages in the midst of recession is salary concessions by the Pittsburgh Symphony Orchestra. A few weeks ago the Orchestra musicians agreed to a not insubstantial 9.7% pay cut next year. In response to their actions, the Symphony's music director, Manfred Honneck, volunteered to take a 10% cut.

While I do not rejoice that circumstances are such that people must accept lower wages, it is good to see people willing to submit to economic reality.

Forty years ago today, the world left the last vestiges of the international gold standard with Nixon's order to suspend gold payments to foreign central banks in 1971. When the British abandoned the gold standard decades earlier, it was foolishly celebrated by John Maynard Keynes.

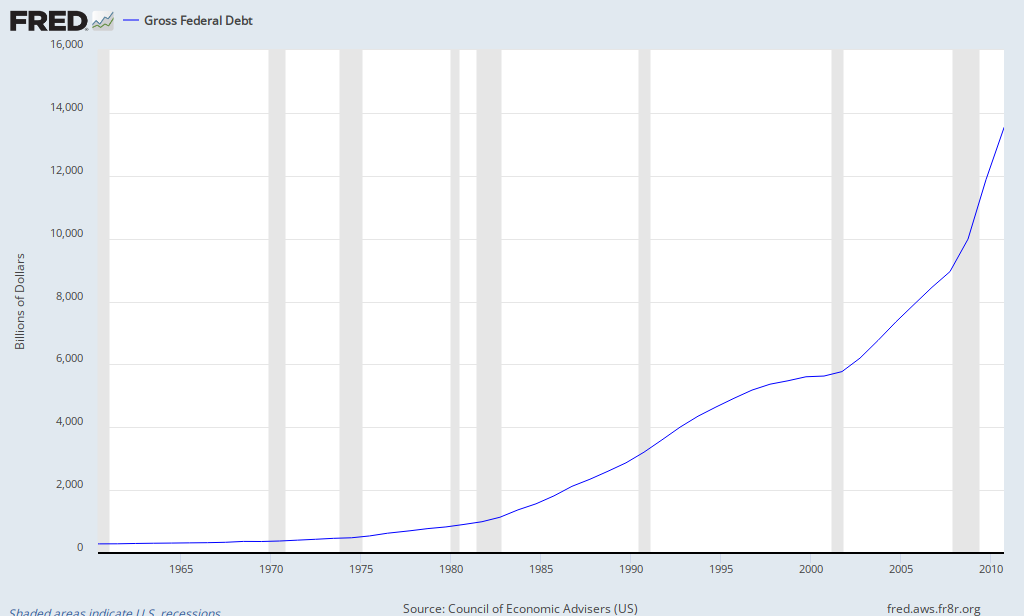

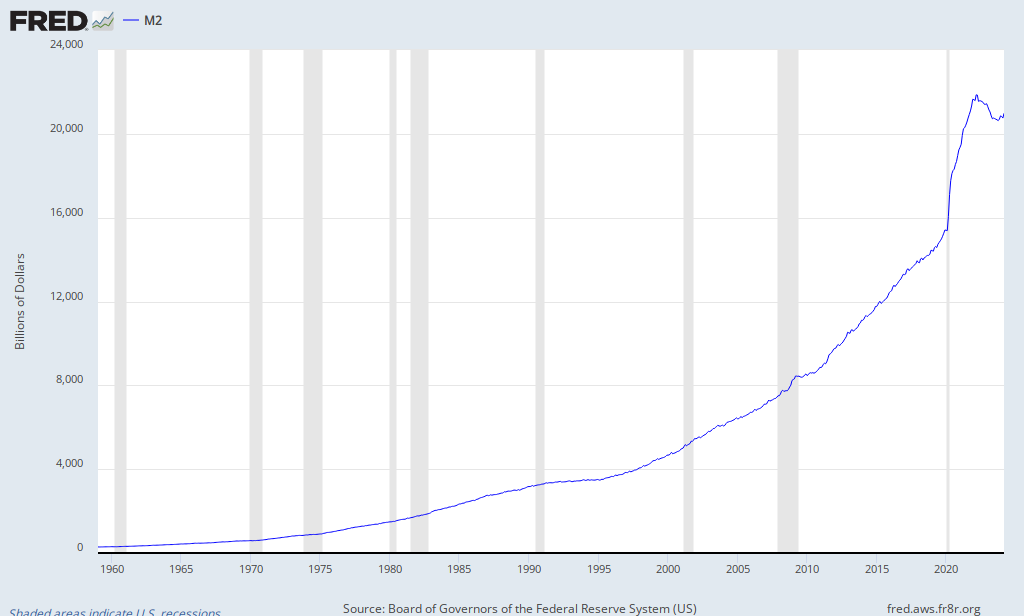

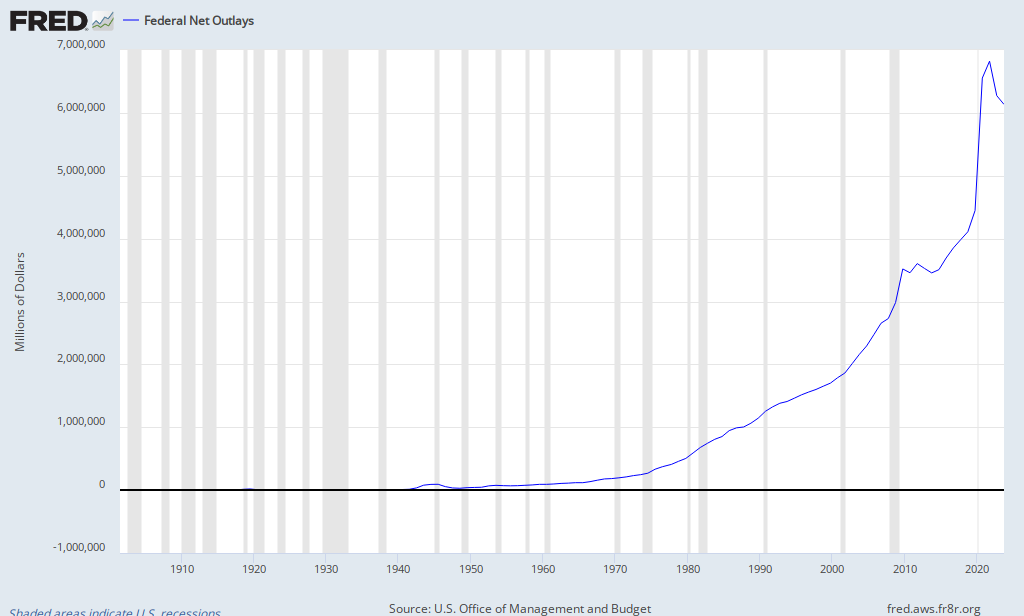

As David Stockman has carefully explained, however, leaving the monetary discipline of the international gold standard ushered in four decades of inflation via artificial credit expansion.The graphs below tell the tale.

Gross Federal Debt began its almost exponential growth shortly after 1971.

The trajectory of the money stock also noticeably shirted upward after closing the gold window.

The increased money stock help fuel massive increases in government spending.

Not surprisingly, consumer prices began to rise faster than ever before after 1971 as well.

A gold standard is not perfect. It will not usher in the Kingdom of God on earth. No mere human institution will do that. What a commodity standard does, however, is to constrain the acts of politicians eager to impoverish the rest of us in order to enrich their friends and themselves. As Mises says in his excellent 1965 essay "The Gold Problem," "The gold standard alone makes the determination of money’s purchasing power independent of the ambitions and machinations of dictators, political parties, and pressure groups."

As Mises has also pointed out to anyone interested in listening,

The gold standard did not collapse. Governments abolished it in order to pave the way for inflation. The whole grim apparatus of oppression and coercion, policemen, customs guards, penal courts, prisons, in some countries even executioners, had to be put into action in order to destroy the gold standard.

The reason Nixon felt compelled to officially abandon the gold standard forty years ago today, was that the U.S. government had been quietly abandoning the gold standard during the sixties. It was doing so by expanding the money supply at a rate much higher that the increase in our gold stock.

As Paul Kasriel documents, from the first quarter of 1952 through June 1971, "the total financial assets of the Federal Reserve, in effect, the amount of credit created out of “thin air” by the Fed, grew at a compound annual rate of 2.81%. But starting around 1964, the golden anchor on monetary policy started to “drag.” That is, growth in total Fed assets accelerated." Between the first quarter of 1952 and December1963, total assets held by the Fed increased at an annual rate of 1.00%. From the beginning of 1964 through June 1971, however, total assets held by the Fed increased 6.09% per year. Too many foreign central bankers began to read the inflationary writing on the wall and began redeeming their U.S. Federal Reserve notes for gold, until it became clear that we would run out if something was not done.

That something was Nixon's closing the gold window. That act moved us to a full fiat paper currency. After the gold window was closed by Nixon, July 1971 through 2003, the annual rate of increase in Fed assets was 7.02%.

Note that there is nothing special, per se, about gold as the monetary standard. I generally us the term 'gold standard' as verbal shorthand meaning any free-market commodity standard. It is possible that if we transitioned into a free market for money production and use, the commodity used as money would be something besides gold; silver for instance. The point is that adopting a free market commodity-based monetary system would help restrain the inflating ways of modern politicians.

Under the Obama administration, the Environmental Protection Agency has proposed and promulgated numerous rules without a complete and accurate assessment of their impacts on consumers, jobs and small businesses. These rules include limits on the emissions of greenhouse gases, more stringent regulations for particulate matter and ozone, and "maximum achievable control technology" standards for power plants. Each will likely raise production costs, reduce economic output and reduce employment in affected industries.

Miller then makes the case for using sensible cost-benefit analysis.

Although levels of ozone and particulate matter permitted under existing standards may be harmful to health, the question arises -- are the benefits of more stringent standards worth the cost, in terms of reduced output, economic growth and employment?

Of course it is hard, when no actual voluntary exchanges occur, to properly assess true costs and benefits. Even if market prices for costs and benefits could be estimated, they are ultimately subjective to the people affected. Nevertheless, Miller's point stands. The EPA should not be an avenue toward despotism.

Ben Bernanke has announced that the Fed will hold interest rates at record lows until at least mid-2013. Predictably stock prices rose. It is clear now more than ever that the Fed sees its job number one as supporting security markets. Damn the malinvestment - Full speed ahead! The markets again put their faith in a man who has been wrong so many times before.

Credit expansion cannot increase the supply of real goods. It merely brings about a rearrangement. It diverts capital investment away from the course prescribed by the state of economic wealth and market conditions. It causes production to pursue paths which it would not follow unless the economy were to acquire an increase in material goods. As a result, the upswing lacks a solid base. It is not real prosperity. It is illusory prosperity. It did not develop from an increase in economic wealth. Rather, it arose because the credit expansion created the illusion of such an increase. Sooner or later it must become apparent that this economic situation is built on sand.

When he says he inherited serious economic problems. The Bush II Administration was an economic disaster, from No Child Left Behind, to massive increases in spending, the creation of a new prescription drug entitlement program, and the first stimulus bill following the financial crisis. Do not forget, however, that Obama asked for the job. Yea, he campaigned for the privilege of inheriting these serious economic problems.

President Obama cannot be judged by what his predecessor did, however, he can and should be evaluated based on his response to these problems. Like Bush II, the Obama Administration has been a disaster on economic issues. It was Obama who signed off on further socializing health care. Obama singed the massive fiscal stimulus bill into law. Obama is now talking about increasing taxes. Obama even reappointed Ben Bernanke for a second term as Chairman of the Federal Reserve. Although we cannot blame our present economic woes solely on our current president, we can blame him for his actions that continues to prolong the agony.

Nothing but debt, says Caroline Baum at Bloomberg. In a very revealing blog post, Mish Shedlock reprints Baum's piece and asks,

Is there any kind of stimulus the US did not try in the last 10 years?

We had 1% interest rates from Greenspan fueling housing.

We had wars from Bush and Obama fueling defense industry employment.

We had two rounds of Quantitative easing from the Fed.

We had cash-for-clunkers.

We had two housing tax credit packages.

We had an $800 billion stimulus package from Congress for "shovel-ready" projects.

We had stimulus kickbacks to states.

We had HAMP (Home Affordable Mortgage Program).

We had bank bailouts out the wazoo to stimulate lending.

We had Small Business lending programs.

We had central bank liquidity swaps.

We had Maiden Lane, Maiden Lane II, and Maiden Lane III

We had Single Tranche Repurchase agreements

We had the Citi Asset Guarantee

We had TALF, TARP, TAF, CPFF, TSLF, MMIFF, TLGP, AMLF, PPIP, and PDCF

We had so many programs the Fed must have run out of letters because they were not given an acronym.

That is a partial list. Other than bailing out bondholders what

exactly do we have to show for any of it? The one-word answer is "debt".

Because debt funded by monetary inflation cannot buy us prosperity, but only make things worse, it is, as Mish says, time to do something different. As painful as it may seem, the government needs to stop inflating (or better yet--End the Fed), reduce spending, reduce business regulation, and remove labor market constraints. In other words, we need to press for a truly free market that will finally allow for liquidation of malinvestment and for a reallocation of factors of production toward their most productive uses (HT: Tom Woods).

In this interview by Gold Money Foundation, the great Jesus Heurta de Soto explains the causes of financial crises and business cycles. He draws upon the theory of Mises and Hayek to explain the cycle.

As he explains,

This financial crisis, the crisis we have experienced in the last at least 200 years, has been caused by a previous process of huge credit expansion that was orchestrated by central banks, and that consists of a process of creation of new money that materialises in demand deposits that are created out of thin air by the banks and given as loans to entrepreneurs so that entrepreneurs will receive the signal that they should invest as if real savings in the society have increased, when in fact this didn't happen. The whole process was financed, as I said, through artificial credit expansion. As a result of that, huge malinvestments were committed and the market, which is a very dynamically efficient process of creativity and discovery, sooner or later discovers these malinvestments, and when the discovery is done, the financial crisis comes.

A friend of mine sent me this video produced by the Post Carbon Institute which is dedicated to "leading the transition to a more resilient, equitable, and sustainable world." The video is written and narrated by Richard Heinberg, author of The End of Growth. He attempts to explain the onset of the Great Recession and why economic growth has not yet returned. You can watch the video below:

I must say I was disappointed with what I saw and heard. Much of what Heinberg says about the proximate causes of the credit bubble and the fictitious prosperity made apparent by debt, is correct as far as it goes. However, he way overemphasizes the importance of our living on a finite planet and energy depletion. For example, Heinberg claims that it was really cheap energy that made the industrial revolution and unprecedented economic growth possible. Given that premise and his belief that we are on the steep downhill slide energy supply wise, it is natural to see the current economic stagnation as the finite earth chickens coming home to roost.

It seems to me, however, that Heinberg just does not give sound economic analysis its due. Certainly the industrial revolution was made possible in part by affordable energy that powered machines. However, that energy had been dormant there since the creation of the world. Why didn't we have an industrial revolution that started the first year after Adam and Eve were created? Perhaps because people had not discovered such sources were useful, because they had no need of them yet?

The causes of the industrial revolution he cites from economists, such as the division of labor, innovation, and increased trade (I would include capital accumulation and entrepreneurial activity), are indeed the causes of economic prosperity. Also, as he argues that economic growth is over, it would be helpful for him to define what he means by economic growth. It seems as if he makes a common error by equating increases in GDP with economic growth. They are not the same thing.

In a free society, people will experience the level of economic expansion they desire in the sense that, given their stock of scarce factors of production, they will act to achieve what they most prefer. Their time preference will dictate how willing they are to save and invest, and, consequently, the magnitude of capital at the disposal of entrepreneurs..

In such an economy, no one will have to arbitrarily tell anyone when is the right time to shift from fossil fuels and no one will be forced to do so against their will. Economic calculation using relative prices will guide people away from more costly energy to energy that is most efficient. Perhaps the true primary underlying cause of our current prolonged economic stagnation is the lack of a free economy. Who knows how prosperous we could actually be with real private property?

This time it is Kevin L. Kliesen and Daniel L. Thornton, Economist and Vice President and Economic Adviser, respectively, at the St. Louis Fed who argue that our increased debt since the 1970s is the result of too much spending. Specifically "the rise in the national debt from the 1970s through 2007 is entirely a consequence of the federal government’s increase of expenditures without an offsetting increase in revenues to pay for that additional spending."

Kliesen and Thornton do argue that the cause of the current crisis is different in that not only has government spending increased sharply during the recession, revenues have also decreased significantly. On the one hand, that is certainly what happened to both government spending and revenue. The fact remains, however, that while the government cannot easily control for decreased incomes and their effect on the tax base during a recession, it has complete control over spending. The current debt crisis is merely a four-decade long spending fueled debt buildup coming to a nasty looking head.

While away on a recent trip I perused the Financial Times during my flight. A letter to the editor struck me:

Sir, As the European Central Bank and the European Commission fight to save the euro, on a rare visit to a McDonald’s in Nîmes, France, this week I thought for a moment that the fight was lost. When I paid with a €50 ($70, £44) note for a Big Mac, the lady at the till promptly started to tear the note in two. In response to my worried inquiry as to what was amiss, I received the reassuring answer that tearing €50 notes was now company policy, at least in this region, to ensure that they were genuine. The metal security strip resists the action.

While my mind was set at rest as regards the immediate survival of the euro, it does suggest that our currency is not perhaps held in the same regard as the US dollar, which I believe is legally protected from such systematic attack.

While it is, perhaps, charming to think that the the U.S. dollar is legally protected from such physical abuse, it's value is surely not protected.

Counterfeiting works to destroy a money's purchasing power by increasing its quantity. As counterfeiters print phoney dollars and spend them, the demand for goods increases, which leads to higher prices and reduces the quantity of goods each dollar can purchase. This can be a real problem if counterfeiting occurs on a large scale.

How big is the problem? The Secret Service estimated that at the end of 2005 $61 million counterfeit dollars were being used and held throughout the world. It is important to remember, however, that the negative consequences of creating money out of thin air occurs no matter who is doing the counterfeiting. $61 million is a lot of money, but it is clear that private counterfeiters are mere pikers compared to the Federal Reserve, our central money creating machine. During 2005 alone the Fed increased the money supply by $107 billion (with a 'b')!

Now you tell me, who has done more to undermine the purchasing power of the dollar: private criminals increasing the money supply by $61 million or the Federal Reserve who increased the money supply by over TEN TIMES that amount in one year?!? In case you are unsure, you might be impressed that the Fed has increased the money supply by $2.5 TRILLION since 2005!!!

James Ballard, President of the St. Louis Federal Reserve Bank, agrees with me that, as far as measurements of price inflation goes, "The Core Is Rotten." In an article taken from a speech delivered in New York back in May of this year, Ballard argues that too much attention is being paid to so-called core inflation, refuting four popular arguments in favor of the core statistic as he goes. I am happy to see a Fed president agreeing with me on the inefficacy of using "core inflation" as a policy guide.

Still, Ballard does not get everything right. As a Fed president he still embraces the Fed's mission to work for stable prices, meaning he still thinks we need a central money making machine to create money out of thin air. He also accepts headline inflation statistics, such as the CPI, as useful measures of the price level. Nevertheless it is nice whenever a Fed President speaks the truth.

A Headline from Bloomberg proclaims "Debt Deal Puts U.S. on Austerity Path as Economy Falters." This assertion, it seems, is the new conventional wisdom. Appealing to the economics of Keynes, Alain Sherter on Bnet faults the U.S. for drinking the "Austerity Kool-Aid." Derek Thompson at The Atlantic asserts that the debt deal is bad for U.S. economic growth because, it allegedly cuts government spending and "government is part of the economy." This conventional wisdom errs for at least two important reasons:

In the first place, the debt deal is not that austere. In fact, it does not cut a single dime in spending. It may plan to lower projected future spending growth, but it does not plan for any true spending cuts. It is a sad, sad commentary on contemporary understanding of political economy when a deal that allows for expanding government debt by $2.4 trillion over two years is greeted with howls of "Austerity!!!!"

Additionally, the idea that cutting spending hurts the economy is as upside-down as the Keynesian economic vision from which it stems. The government, contrary to the conventional wisdom, is not part of the productive economy. The government is a great consumer, but not producer. It is only by confusing GDP with the economy, that someone can believe that as government spending goes, so goes the economy. To the extent that the state gains revenue from anywhere it must take from the productive. Government spending merely takes scarce economic goods out of the hands

of private entrepreneurs and capitalists and transfers them to the government bureaucratic

class. There is no reason to believe that bureaucrats have either the ability or incentive to allocate scarce goods in productive investment. As I have said before, and no doubt will say again, government money cannot buy prosperity.

The exact opposite is true. Contrary to the new conventional wisdom, the lower government spending is, the better off our economy will be. With less government spending, the state will need to tax, borrow, and inflate less. Lower taxes, borrowing, and less monetary inflation, will both encourage saving and investment, which is the true source of sustained economic progress. Lower monetary inflation also will reduce distortions and malinvestment in the economy that are due to artificially lower interest rates and price changes that do not reflect economic reality. Even better macroeconomic policy would include cutting taxes and slashing spending enough to balance the budgets through spending cuts. It would also include ending the Federal Reserve altogether and move to a free market in money production.

When the deal is the "historic" and "dramatic" agreement just passed by the U.S. House of Representatives. Gregg Easterbrook in an outstanding column on Reuters very ably explains why this "historic" debt reduction deal is "as phony as a three dollar bill."

Easterbrook explains that there is no actual saving or spending reduction in the entire bill.

The closest thing to a tangible “saving” in the agreement is $1 trillion in caps on discretionary programs, spread over 10 years. The new national-debt ceiling allows borrowing to rise by $2.4 trillion, with a plan to pay back less than half that amount over 10 years.

Get it? A huge surge in spending now is called a “spending cut,” while actual cuts don’t take effect for up to a decade. And that’s setting aside that inflation means the present value of money spent today sharply exceeds the value of smaller cuts many years in the future.

Easterbrook also notes that the debt ceiling is not a ceiling, because it always gets pushed up, this time around by $2.4 trillion!

The deal raises the federal borrowing ceiling by $2.4 trillion. This means Congress will immediately spend another $2.4 trillion. That basic point is being overlooked.

You’ve got a debt ceiling on your credit card. The ceiling is there for emergencies, and all responsible borrowers work to stay below their credit ceilings. Experience with the national debt ceiling, by contrast, shows that every dollar of available debt is always spent. Announced in doublespeak as a “savings” plan, this deal guarantees the national debt will rise another $2.4 trillion. The moment the deal becomes law, members of Congress from both parties will see an added $2.4 trillion in the cookie jar and begin raiding.

The entire piece is worth reading, thinking upon, and sending to your friends. Nota Bene: Not recommended for those with high blood pressure.

It will merely allow slower growth in government spending than our rulers desire. It begs Peter Klein to consider the nature of a Krugmanian slasher-flick.

It turns out that the last time that federal government spending decreased from one year to the next occurred during the final year of the Truman administration. From 1953 to 1954 spending fell from $76.1 billion to $70.9 billion.

Hazlitt was also provides a more accurate assessment of the economic efficacy of the WPA. "When we had our WPA, it was considered a mark of genius for the administrators to think of projects that employed the largest number of men in relation to the value of the work performed--in other words, in which labor was least efficient" (p. 72).

Hazlitt was also provides a more accurate assessment of the economic efficacy of the WPA. "When we had our WPA, it was considered a mark of genius for the administrators to think of projects that employed the largest number of men in relation to the value of the work performed--in other words, in which labor was least efficient" (p. 72).